Remodeling? Don't Get Caught with Your Pants Down.

Make sure your contractor has a Certificate of Liability Insurance

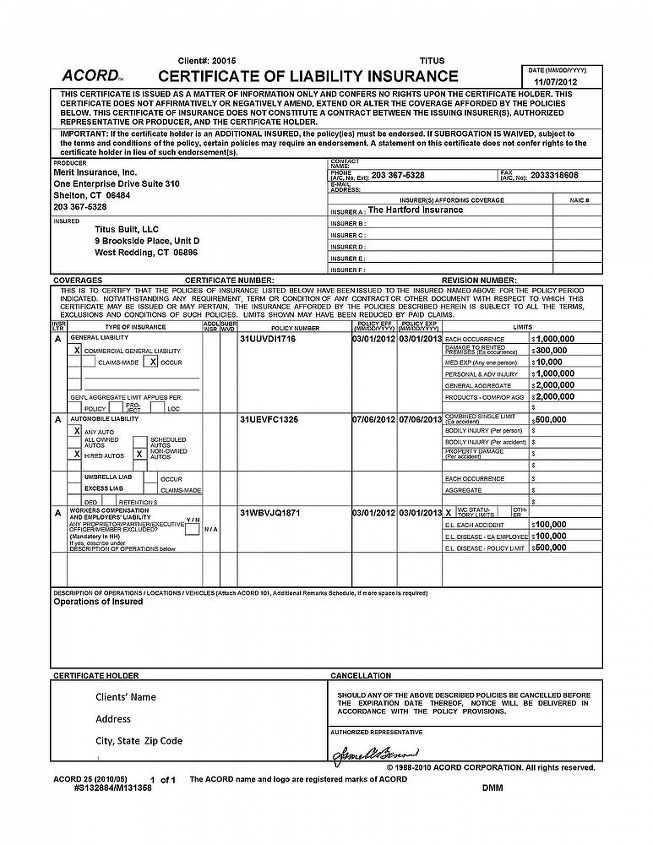

Homeowners, beware: nobody should step on your jobsite without a Certificate of Insurance which has been checked and verified! If you are doing business with a service company that will be working on your premises, you should first make certain that the company has sufficient liability insurance. If work will be performed by the company's owner himself, without other employees, a general liability policy is sufficient. However, if the owner has employees that will be working onsite, workers' compensation insurance is required.

The best way to obtain the Certificate is to have the service company's insurance broker forward the Certificate to you. The Certificate should name you, with the jobsite address, as the Certificate Holder and should name you as the "additional insured." This Certificate will give you proof that coverage is valid, as well as provide you with protection for yourself and 3rd parties in the event a 3rd party sues you due to negligence of the contractor. It will also inform you of the amount of insurance coverage provided so you may determine whether or not the coverage is sufficient for your needs. (For more information, contact your insurance broker.)

Note: In addition to the Certificate of Insurance, homeowners should have a written contract with the contractor which includes "hold harmless" language protecting the homeowner. If a claim is reported and the service company has not provided you (the homeowner) with a Certificate, the claim will go directly against you. If your insurance policy does not cover service companies, the cost of the claim will come directly out of your pocket.

Homeowners, beware: nobody should step on your jobsite without a Certificate of Insurance which has been checked and verified! If you are doing business with a service company that will be working on your premises, you should first make certain that the company has sufficient liability insurance. If work will be performed by the company's owner himself, without other employees, a general liability policy is sufficient. However, if the owner has employees that will be working onsite, workers' compensation insurance is required.

The best way to obtain the Certificate is to have the service company's insurance broker forward the Certificate to you. The Certificate should name you, with the jobsite address, as the Certificate Holder and should name you as the "additional insured." This Certificate will give you proof that coverage is valid, as well as provide you with protection for yourself and 3rd parties in the event a 3rd party sues you due to negligence of the contractor. It will also inform you of the amount of insurance coverage provided so you may determine whether or not the coverage is sufficient for your needs. (For more information, contact your insurance broker.)

Note: In addition to the Certificate of Insurance, homeowners should have a written contract with the contractor which includes "hold harmless" language protecting the homeowner. If a claim is reported and the service company has not provided you (the homeowner) with a Certificate, the claim will go directly against you. If your insurance policy does not cover service companies, the cost of the claim will come directly out of your pocket.

Titus Built, LLC Certificate of Liability Insurance

Want more details about this and other DIY projects? Check out my blog post!

Comments

Join the conversation

2 of 12 comments

-

Great information Sharon. One more point. Be sure that the name of the insured contractor is also the contractor's entity name on your contract. If you contract with Joe X Construction LLC, that should be the name on the insurance certificate. Not Joe X or Joe X Construction Company.

-

We run into this problem quite often with the subs. The Certificate states one name and their invoice states another name. I always tell the subs to send me the Certificate in the name on the invoice or else I will have to cut the check under the name on the Certificate.

Frequently asked questions

Have a question about this project?